Table of Content

- Credit Unions

- Quick & easy online application

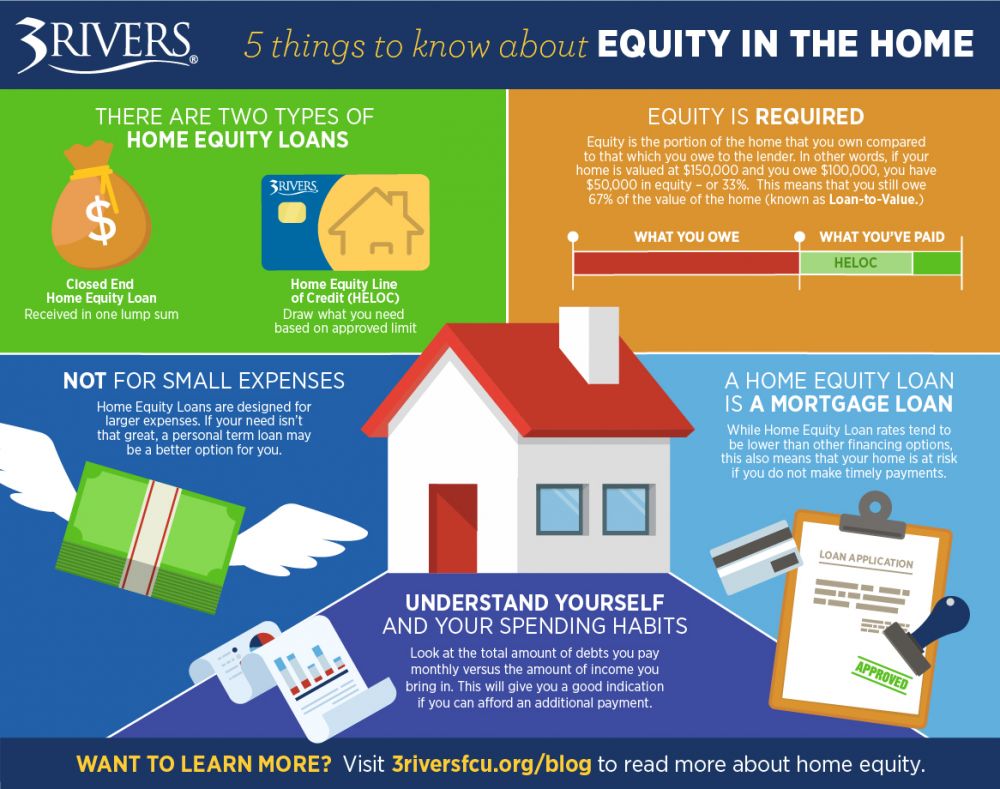

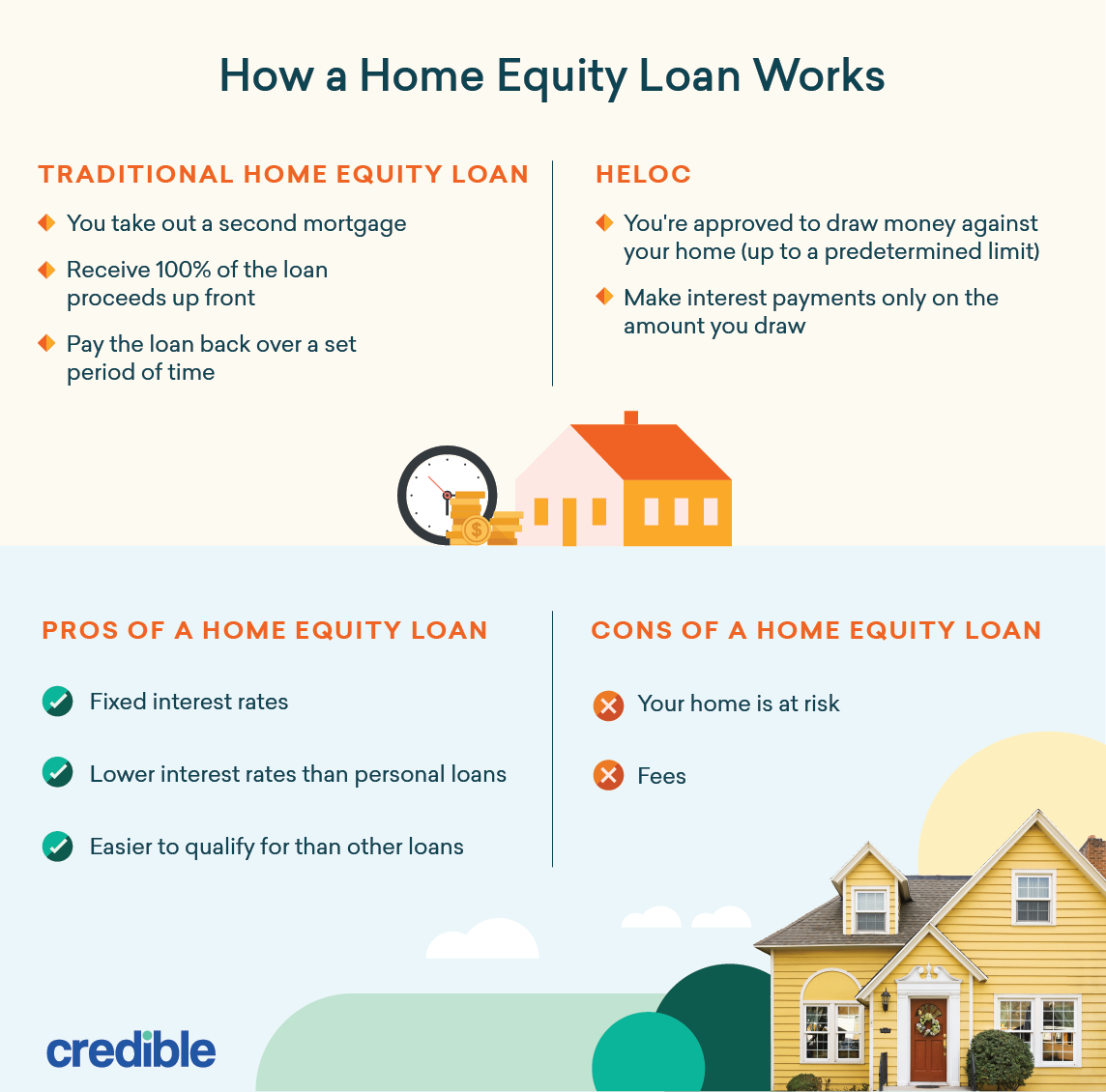

- Pros of home equity loans

- Cons of a home equity loan

- Up to 95% LTV with a HELOC Combo Financial Markets Mid-back Office

The bank also allows you to get a “loan estimate” in real time, which would include the estimated interest rate, monthly payment and total closing costs. Other details—such as the minimum credit score required and average time to close a loan—are not readily available, and the bank did not respond to requests for information. A 15-year mortgage refinance has some advantages, too, namely that you pay a lot less interest over the life of the loan. Fifteen-year mortgages tend to charge lower rates than 30-year mortgages, and they also have a shorter repayment window, so the overall savings can be significant. Remember, though, that a short repayment window is a double-edged sword.

Outside the digital world, Marc can be found spinning vinyl, threading reel-to-reel tapes, shooting film with his Bolex and hosting an occasional pub quiz. If you aren’t sure how much money you need, a home equity line of credit may be a better choice for you. They are revolving forms of credit, so you can tap into them again and again during the draw period. Instead, using a home equity loan—and leaving your existing mortgage in its current state—may lower your overall repayment cost. Our experts have been helping you master your money for over four decades.

Credit Unions

Our site provides links to third party sites and resources not controlled or operated by A+FCU. Other websites may have privacy policies, security, and terms of use that aren’t the same as A+FCU’s. A+FCU isn’t responsible for third party content, agreements, or transactions on linked sites. If you’d rather not continue on to this site you can always call us or stop by a branch to find out more.

The content created by our editorial staff is objective, factual, and not influenced by our advertisers. Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information.

Quick & easy online application

Although home equity loans have higher rates than mortgages, they usually have lower fees. That’s because you have to pay closing costs as a percentage of the entire loan amount. HELOC rates start a 4 percent APR if you pay $400 for discount points. Otherwise, rates start at 4.25 percent APR, which comes with a $500 credit toward closing costs. Lower’s HELOC has a five-year draw period and a repayment period ranging from five years to 20 years. Founded in 2018, Lower is a direct mortgage lender that is part of Homeside Financial.

It may have an extra incentive to offer you a lower rate or some reduced fees in hopes of keeping your business. Home equity loans typically have fixed, rather than variable, interest rates, so once you've signed up for one, your payments should be predictable and not result in any unpleasant surprises. Lower® and its DBAs provide home loans; Lower Realty, LLC provides real estate services; Homeside Insurance Services, LLC facilitates shopping experience for homeowner’s insurance policies. No matter which option you choose, refinancing with Lower can save you money. Although home prices rose more than 42% since the beginning of the pandemic, the impact of rising mortgage rates is starting to show as home prices begin to decline. If your property loses value and is worth less than you paid for it, and if you've taken out a home equity loan in addition to your mortgage, you could end up with negative equity.

Pros of home equity loans

If you’re planning home renovations or a vacation, create a budget—and add some wiggle room to give yourself some cushion. Main First, calculate the amount of equity you have in your home and how much you can borrow using our Loan Amount Calculator. Customer support by phone is available Monday through Friday from 8 a.m. Customer support is available by phone Monday through Friday from 8 a.m.

The credit union also allows you to borrow up to 100% of your CLTV for a first and second home, which is higher than most competitors. Credit unions require a membership, but many have broadened the rules so that almost anyone can join. Before you jump through any hoops to join a credit union, though, check the interest rates it has available.

Cons of home equity loans

The lender offers quick approval and closing, as well as competitive APRs. Home equity loans allow homeowners to borrow against the equity in their homes. Equity is the difference between your home’s value minus what you owe on your mortgage. Tapping your equity through a home equity loan is just one way to access it, and unlike some types of loans, it will allow you to get the full amount upfront.

The lower rate also requires automatic withdrawals from a TD Bank checking or savings account. Starting APRs are based on borrowers having the best credit profiles and applying for an LTV of 80% or less. It also includes a 0.25% initial rate discount when a borrower sets up automatic payment from an Old National checking account.

If you can’t get better terms or a lower interest rate than what you have on your existing debt, keep looking at what other lenders offer. Having a plan for how you’ll attack high-interest debt — and how you’ll repay your home equity loan — can set your finances up for a more secure future. Generally, you’ll need a credit score of at least 620 to qualify for a home equity loan, but some lenders offer this type of loan even if you have a lower score or bad credit. This assumes, however, that you have adequate equity in your home and a lower debt-to-income ratio, preferably under 43 percent. If you’re seeking a home equity loan to consolidate debt, the latter might not add up for you. One option is to work with the lender that originated your first mortgage as you already have a relationship and history of on-time payments.

The lender approves the HELOC at a 5.5% variable interest rate with a 10-year draw period, followed by a 20-year repayment period. You hire the contractor and draw funds from the HELOC as needed to pay for the work. Your minimum payments during the draw period are interest only . Once the draw period ends, you pay both interest and principal.

Extending the term of your loan means lower monthly payments, which can free up some money if you have a tight budget. Monthly payments on a 10-year fixed-rate refi at 5.97 percent would cost $1,108.70 per month for every $100,000 you borrow. That's a lot more than the monthly payment on even a 15-year refinance, but in return you'll pay even less in interest than you would with a 15-year term. With a home equity loan, you receive the entire loan amount as a lump sum payment with repayment terms set to a fixed interest rate over a specified length of time.

A HELOC is a revolving line of credit that typically has a variable interest rate. Let’s give your home equity more time to grow—you’ll need $25,000+ in home equity to be eligible. With a HELOC, you’ll be able to draw on the available funds and use that money as needed.

No comments:

Post a Comment